A Reasonable Approximation

Latest posts

Walkthrough: Filing a UK self-assessment tax return

I'm writing this guide for a few reasons. For one, it might be useful to someone, possibly me in future. For two, if I make a mistake, someone might call me out on it and then I can correct it. And for three, it gives me a venue to complain about things I think aren't very good about the online submission form and also our tax system.

(Overall I'm pretty positive on the form! I'm gonna complain a lot, and I'm not going to point out all the places where it works and the instructions are clear and easy to follow. So this will probably come across quite negative, but that's because I'm counting down from perfection, not counting up from zero.)

Most people in the UK don't have to file one of these. I started filing them when I started earning in the 40% tax bracket. I'm not sure I still have to - I think I got a message a year or two back saying I could stop - but if I don't I'll pay more tax than I need to.

HMRC publishes a document called "how to fill in your tax return". (In previous years it had the reference SA150, and that's still in the filename, but it's no longer written under the title for some reason.) I actually haven't found it very helpful, it mostly doesn't seem to answer questions that the website leaves me with. But I guess it might be helpful in theory.

Update December 29: I only know about the parts of this process that are relevant to me. Some questions about other parts are answered in the comments on /r/UKPersonalFinance. Also, I generally find that community to be very helpful and knowledgable, so I find it reassuring that they only caught one mistake so far.

The gov.uk page on filing says you have to register first unless you sent a tax return last year. I've sent tax returns for several years running now, and I don't remember what registering was like.

Logging in from there I get sent to my "personal tax account" page and click the "complete your tax return" link in the top right box. I feel like that was harder to find in the past. It explains who can and can't file a return, I assume I read that in a previous year and could then and still can, and I click 'start now'.

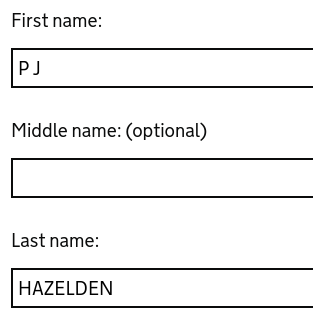

The first page has a bunch of stuff filled in for me, mostly accurate.

"P J" is my first two initials, not my first name, but nice try. The all-caps HAZELDEN seems unnecessary, you don't need to worry about my handwriting.

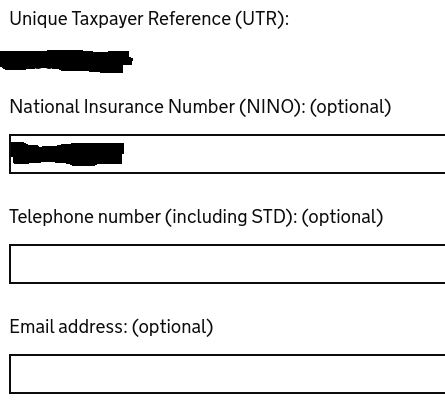

These say 'optional', which sounds like I don't need to give them if I don't want to. But up above it says

'Optional' indicates only complete if relevant to you

So maybe that means "give us this if you have one"? I'm probably safe to leave out my phone number, I don't want them calling me and I don't know what "STD" means.1 I'll grudgingly give them my email address I guess.

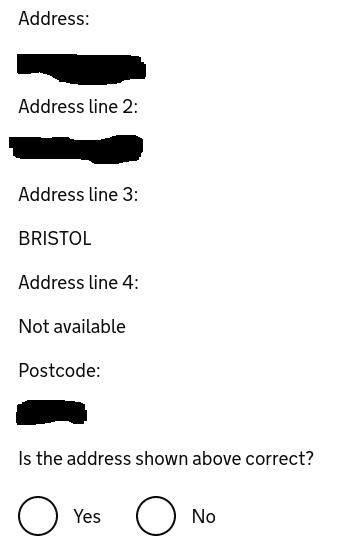

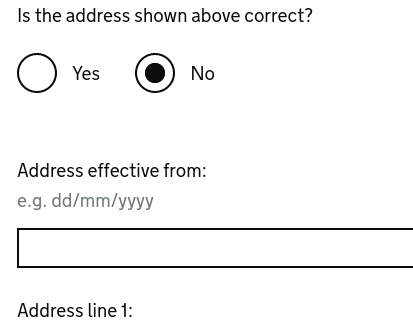

For years I've been using my parents' address for all official stuff, which is easier than telling banks and the like every time I move house. But some time this year I got a scary letter telling me I had to register for the electoral roll in my current place, which meant I got removed from it back in Bristol. So probably I have to give my current address here too.

(I don't see why it's any of the government's business where I live. Unfortunately they disagree, and they have all the power in this relationship.)

Well this is awkward. I moved in here in 2019, but I wouldn't have given this address when filling in my 2019-20 tax return. Will they get pissy with me if I give the date I moved in? Eh, probably not.

Almost every address form I've filled in for the past several years has let me give my postcode and then select my exact address from a short dropdown, or enter it manually. This address form does not offer that.

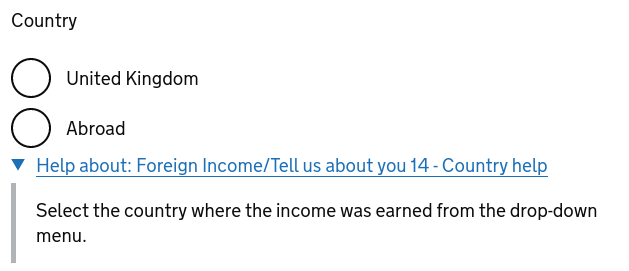

There's no dropdown box, even if I select "Abroad". Also, this is still supposed to be asking about my address - "where the income was earned" is a different question. (And not a very clearly worded one, what if I earned income in multiple countries?) Fortunately I have never lived or earned income outside the UK.

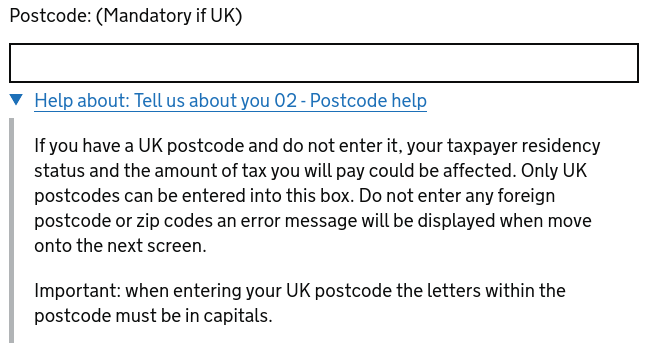

"The postcode must be in capitals." Well done for finding and documenting a bug, HMRC, but I feel like it shouldn't be too hard to fix this one.

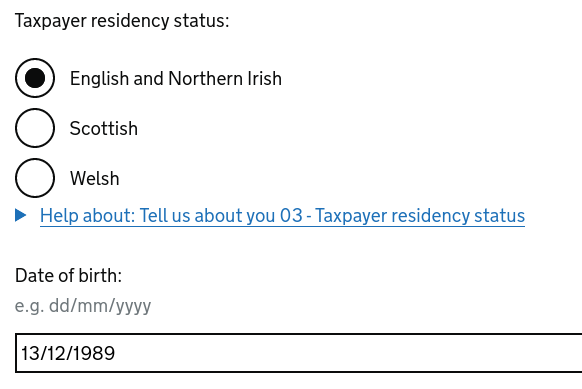

Residency is "based on whether you lived in England and Northern Ireland, Scotland or Wales for the majority of the tax year". I assume they mean "plurality", but maybe if you spent less than half the year in any of these, you don't pay tax at all. (Tax collectors hate him! Nonlocal man discovers one weird trick…)

That's not what "e.g." means, but the date is correct.

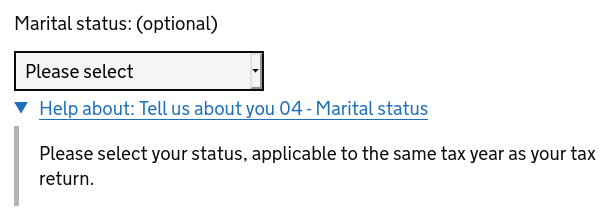

This is 'optional', so maybe there are people who don't have a marital status, as distinct from having the marital status 'single'? Or maybe, contra what they said above, it means I don't have to tell them, and then probably they'll treat me as single if I don't specify?

The options are: Single, Married, In Civil Partnership, Divorced, Civil Partnership dissolved, Widow, Widower, Surviving Civil Partner, Separated. Obviously you can be more than one of these in any given tax year, or even more than one of them simultaneously, so the help text is not very helpful. I guess the idea is you give the most specific version of the most recent change as of the end of the tax year? I don't know who would ever pick "separated". Luckily for me, the government hasn't decided it cares about long-term cohabiting relationships until we actively make them legible, at least not for tax purposes. So I get to just say "single" and not worry about it.

This is the only part of the tax return (at least the pages I saw) where your gender becomes relevant, and then only for widows and widowers. I don't know what the nonbinary version is, but they get left out.

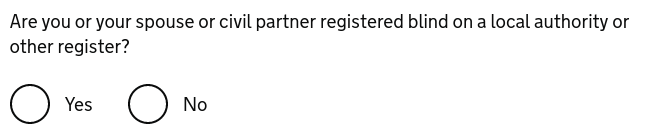

If they're assuming I didn't move house, you'd think they could assume I didn't go blind or get a blind spouse or civil partner.

I wonder what counts as an "other register". I think it's a crime to lie on my tax return, and quite possibly a crime to lie to my local authority about being blind. But it might not be a crime to lie on Honest Joe's Register Of Definitely Actually Blind People, and then to truthfully tell HMRC that I'm on that register. (This sounds like the sort of thing that you patiently explain to a judge and then the judge adds a little extra to your fine for being a smartarse. You try to appeal and the appeals court rejects with the comment "lolno". If you're going to try this, I think the funniest way would be to borrow a guide dog to take to court with you, maybe carry a cane slung over your shoulder, but make no actual pretense at blindness.)

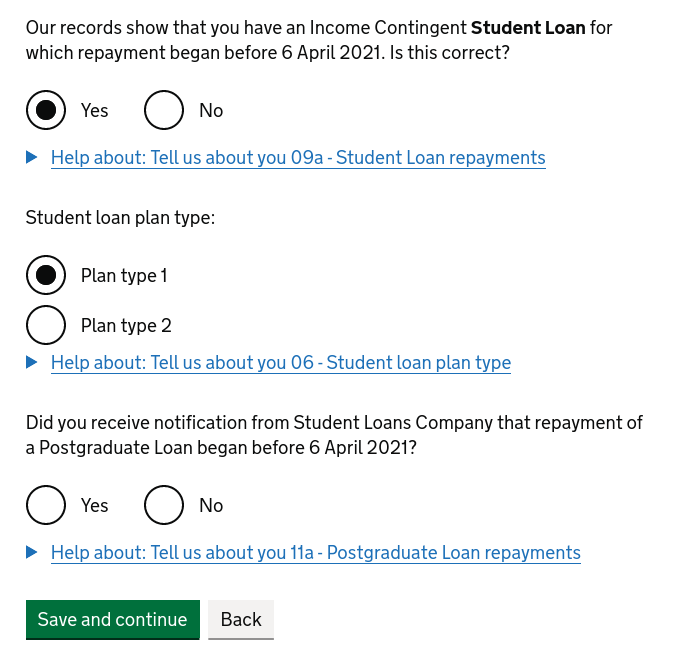

There's nothing here telling you how to figure out if you're on plan 1 or plan 2, but I am indeed on plan 1. The Student Loan Company told them that (according to the help text), but apparently didn't tell them enough to know that I do not have and am not repaying a postgrad loan.

The next page helps figure out which other pages should be included in the rest of the form, and which ones can be skipped.

In my case, I was an employee (or director or office-holder) during the tax year, so I answer yes and tell them how many employments (or directorships) I had (one) and the name of the employer.

I wasn't self-employed or in a partnership, but if I was I'd need to tell them how many of those I had and their names, too. I didn't get income from UK land or property over £1,000 (or indeed at all), I didn't receive any foreign income, and I don't need to complete the capital gains section.

For capital gains it's not entirely obvious that the answer is no. Here's the advice:

You must report your capital gains and attach your computations if in the tax year either:

- you disposed of chargeable assets which were worth more than £49,200

- your chargeable gains, before the deduction of any losses, are more than £12,300

- you have gains in an earlier year taxable in this period

- you want to claim an allowable capital loss or make any other capital gains claim or election for the year

In working out if the assets you disposed of were worth more than £49,200 use the market value of any assets you gave away or sold for less than full value and ignore disposals of:

- exempt assets such as private cars, shares held within Individual Savings Accounts

- assets to your spouse or civil partner, if you were living together at some time during the tax year

- your own home where: [omitted a sub-list because I don't even own a home]

In working out your total chargeable gains include any gains attributed to you, for example, because you're a settlor or beneficiary of a trust, or in certain cases where you're a member of a non-resident company.

This is fairly readable, but it keeps using words like "chargeable" and "allowable". Those sound like they have important technical definitions. Are we given the important technical defintions? Ha, no.

So here's my current understanding. I have shares in some index funds in ISAs and pensions, but I'm pretty sure I should ignore those. And I own a handful of individual stocks and cryptocurrencies, not in tax-protected accounts, that I shouldn't ignore.

But so far all I've done is buy things and let their values go up or down. I haven't "disposed of" any of them: sold, traded or given away.2 That means I don't need to worry about it. When I dispose of something, I'll need to work out how how much profit or loss I made on it, and also (as a separate question) how much it was worth at the time. If those amounts go over certain thresholds in total for the year (£12,300 and £49,200 respectively), then I need to fill in the capital gains section. And there's also another two reasons I might need to, but I'm confident those don't apply to me either.

So I can answer "no" to capital gains because I haven't disposed of anything. Also, outside of ISAs and pensions I had less than £49,200 and my on-paper gains for the year were less than £12,300, so I could answer "no" even if I'd sold everything at the end of the year.

(Also, something unclear: to calculate gains, the obvious thing is to take "price when disposed of" and subtract "price when bought". And we're calculating "price when disposed of" anyway. But we're told to ignore certain disposals when calculating the total disposal price. Do we also ignore those disposals when calculating gains? I would guess so, but mostly I'm glad I don't have to worry about it.)

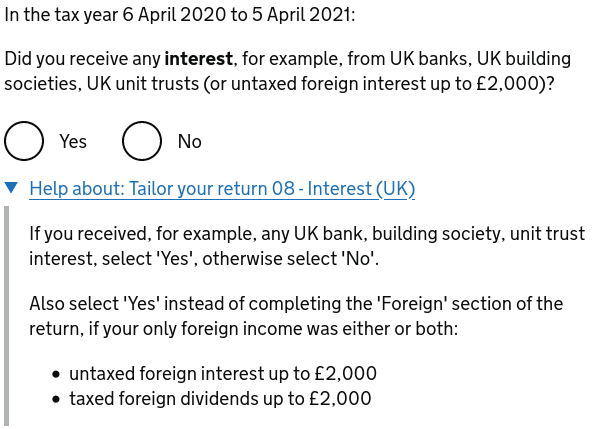

The next page is the same sort of thing, but in my case less clear.

An important detail here is that you can omit interest earned in an ISA. Nothing on the page says so. You might think that if you only earned interest in an ISA, you say here that you earned interest, and later you tell them it was only in an ISA. At any rate, that's what I thought the first time. But then they told me I owed tax on all that interest, so I decided to go back and tell them I didn't earn any interest.3

I guess that was lying on my tax return, and I just admitted to a crime? Thanks, HMRC.

(I just double checked: if I say I did earn interest, I get a new page where they ask me about "interest that's already been taxed", "interest that hasn't yet been taxed", and "foreign interest that hasn't yet been taxed". There's nothing on that page, either, saying I can omit ISAs.)

Similarly, dividends earned in an ISA don't count here. I did not earn any dividends outside of an ISA last tax year. (This tax year I've earned about £1.50 of them so far.)

Ever get the feeling that someone said "every question needs help text" and the person writing the help text was phoning it in?

I don't know how Child Benefit works. Is anyone in the position of "I got it during the tax year starting on 6 April 2020, but the payments had stopped before 6 April 2020"?

This seems to be an "if you made a mistake, that's fine, you can correct it now" thing. I appreciate that.

This help text is long so I'm not including it. This includes casual earnings, and I might have had some of those? Certainly I have in other years, like the money I sometimes got for getting my brain scanned. But it says I don't need to report if the total from this plus self employment is less than £1,000, which it is for me.

They don't mention gambling income, and mine isn't that high anyway, but I think that should be excluded.

I don't know what these are and the help text doesn't help much, but probably not.

Again, long help text. But the gist seems to be that if I have more than £1,073,100 in pensions in total (5 significant digits! Impressive precision), or if I (or my employer) put more than £40,000 into pensions this year, I need to worry about this. Neither is the case for me. (Yet! Growth mindset.)

One more page of basically the same thing, but this one is easy again. Yes, I contributed to a personal pension. Yes, I gave to charity (and claimed gift aid). My partner and I are ineligible for married couple's allowance (we are neither married nor in a civil partnership, and anyway we were both born after 6 April 1935). Nor can I transfer 10% of my personal allowance to them (we are neither married nor in a civil partnership). I don't want to claim other tax reliefs. I don't have a tax adviser. I… think I haven't used any tax avoidance schemes, but that probably relies on distinguishing between schemes that HMRC thinks are legit (like giving to charity) and schemes that HMRC thinks are kinda sus. I haven't used any disguised remuneration avoidance schemes. I am not acting in capacity or on behalf of anyone else.

There is one interesting one here.

I got a tax rebate in tax year 2019-20 from 2018-19, and then another in tax year 2020-21 from 2019-20. I think neither of these is what it's asking about. Rather, I think this is asking about rebates in tax year 2020-21 from tax already paid in that tax year.

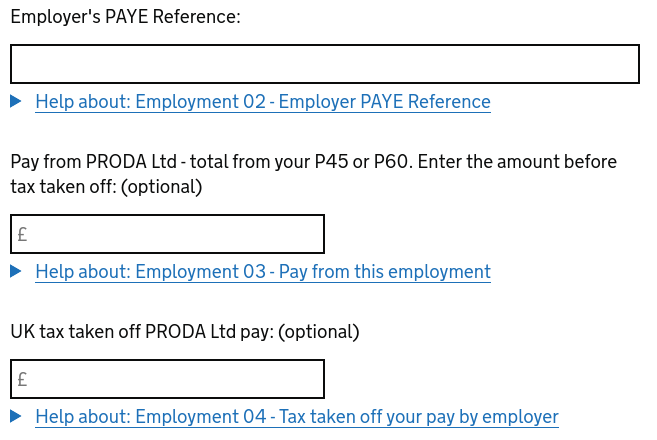

Having filled in those three pages, I get an overview page listing what I've filled in so far and what I still need to do. The first thing to do is income. I only had one employer this year, so I only have one section for that.

They start with the company name, that I already gave them but I can change it now if I want I guess. After that, the next three questions are answered by my P60, which I was able to find because my employer emailed it to me.

These last two are "optional". First time I did this, I thought that meant "we have a copy of your P60 too, so if you don't fill this in we'll fill it in for you". Nope, it means "if you don't fill this in we'll think it's 0".

Then they want to know if I got any tips or other payments not on my P60, which I didn't. This one is optional too - if I try to enter 0 it complains and tells me to leave it blank.

Also, some helpful Javascript on the page makes sure your numbers are given to two decimal places, i.e. pounds and pennies. You can't enter pennies, they'll be truncated (£567.89 becomes £567.00), but it makes sure to show you them.

They also want to know if I was a director (no) and something about "inside off-payroll working engagements" (not entirely clear what this is, but no).

I did have benefits, medical insurance. The value of that will be on my P11D, not my P60, but they don't ask for it here. That's on the next page, which I guess I won't get shown if I didn't have any?

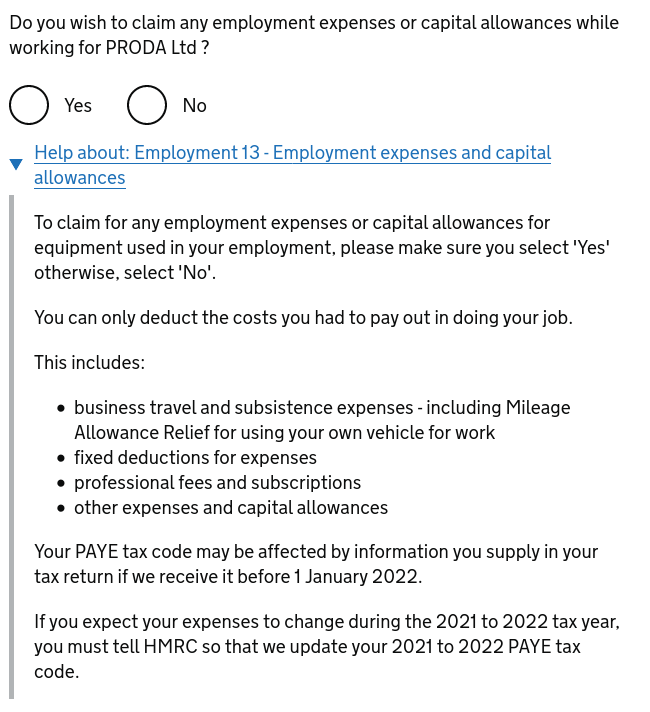

The final question almost caught me out:

I don't normally think of myself as having employment expenses. But I've been working from home, and this is how I claim back some of my utility bills.

My answers to that question added two new pages that weren't listed on the overview before. First for taxable benefits and expenses, listed on my P11D. I have an email copy of that too, I just copy the amount listed for medical insurance on that into the "private medical or dental insurance" box on the page.

They even tell me which number to use. (I have three, "cost to employer", "amount made good or from which tax deducted" and "cash equivalent". The middle one is £0 and the others are equal, so it's not hard for me. But if the middle one wasn't £0, I wouldn't be sure whether to use "cost to employer" or "cash equivalent" - but the latter is the one labeled with an "11", so that's the one to use.)

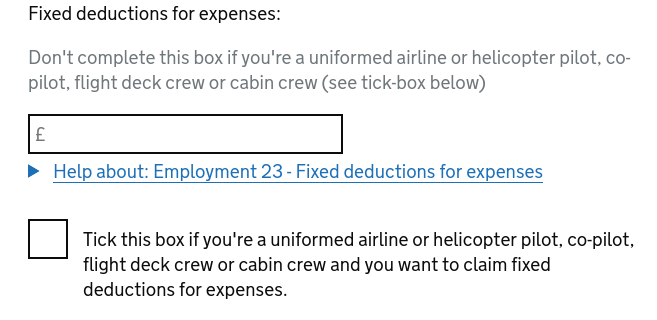

Then there's a page for expenses not reimbursed. The weirdly specific thing on this page is the box for "fixed deductions for expenses":

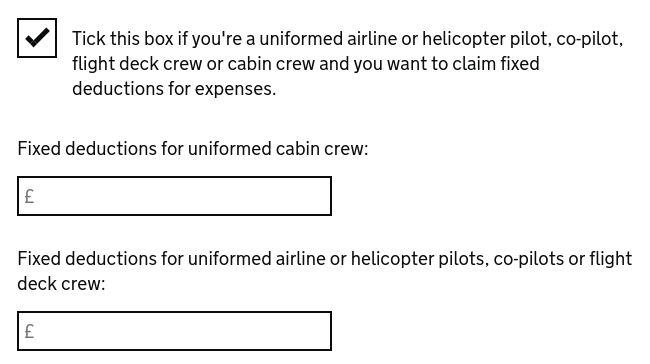

Based on the (long) help text, this seems to be "people in certain jobs and industries get to put specific numbers here, regardless of what their actual expenses were". (But they can choose to instead put their actual expenses in another box.) But if you're "a uniformed airline or helicoptor pilot, co-pilot, flight deck crew or cabin crew", you get a different box to put specific numbers in.

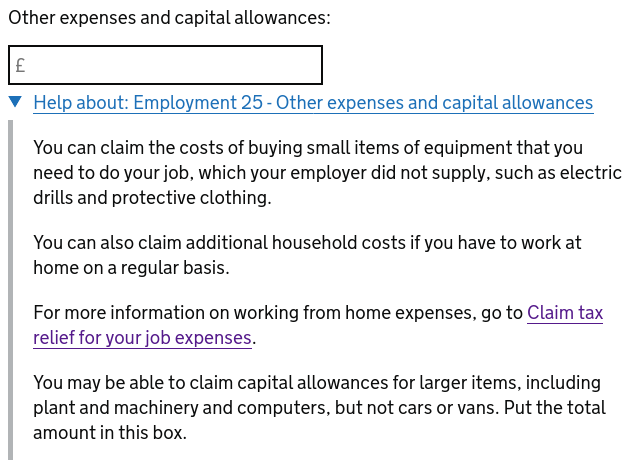

But as far as I know I do not work in such a job or industry. The only question relevant to me is "other".

The help text doesn't make it clear how much I can claim, but the link mostly does. I can claim for gas, electricity, metered water, business phone calls and dial-up internet4; but only the amount of them that's related to my work. So I guess I should figure out how much higher my bills are WFH than they would be if I was in the office?

I can claim up to £6/week without evidence, or more with evidence.5 I can only claim if I have to work from home, not if I do so by choice. I had to look this up, but there were four months where my office was closed (April, May, June and November), so call it 16 weeks. It's also not entirely clear whether that's "£6/week no matter how much I had to work from home that week" or whether I should think of it as £1.20/day, but that doesn't affect me personally. I assume I shouldn't count any holidays I took, but I don't think I took any in those months.

Same-day update: Reddit user pes_planus points out that if you had to work from home for a single day due to Covid, you can claim for the whole year. At £6/week, that's £312 in total. This is the case for both 2020-21 and 2021-22.

Following this page there's one for providing any more information.

I'm not sure what kind of thing I'd need to use it for, but I don't have anything to add. Which is good because it's kind of embarrassingly limited. I'm not allowed to use multiple lines or most punctuation?!

Next up is pensions. I have two pensions that I contributed to this year, my employer one and an SIPP. I'm not aware of having a retirement annuity contract whatever one of those is, and I don't have any overseas pensions, so there are only one or two questions relevant to me. Still, this page is frankly confusing.

I have a standing order to deposit into my SIPP every month, and then about 11 weeks later, 25% of that amount gets added as tax relief. (It's supposed to be 6-8 weeks, but it's not.) So do I count the tax relief in the tax year when it arrived, or the tax year when I deposited the money? So far I've been doing when I deposited, and that's what they suggest by telling me to multiply the amount I contributed by 1.25. On the other hand, if that calculation is always correct, why don't they save me the trouble and do it for me? (Maybe they expect me to have a document somewhere giving the total amount?) In any case, there's nothing saying explicitly what to do. It probably doesn't make that much difference as long as I'm consistent year-on-year, so let's stick with "deposited".

Meanwhile, my employer pension has two sources of contributions. There's the stuff "my employer pays", which doesn't get written on my payslip, and the stuff "I pay", which does. These are both part of my compensation package, but I think we like to pretend that if my employer doesn't write it on my payslip it's not causing me to get paid less? And we make things more complicated and less transparent in service of this fiction.

Anyway, the stuff "my employer pays" I think isn't relevant here. The stuff "I pay" is. In my case, this is also paid relief at source, meaning it's deducted after I've paid tax on it. So that sounds like it matches "Payments to your employer's scheme which were not deducted from your pay before tax". Buuut… I think that question is trying to ask about payments which were expected to be deducted before tax. At my previous job that's how it happened, and it sounds like under certain circumstances that could have gone wrong and then I'd use this question to correct that.

So I think contributions "I paid" to my employer pension actually go along with my SIPP contributions as the answer to the first question, and I leave this one blank. (It's not marked optional, but it doesn't accept 0.)

For charity, there's three questions that look maybe relevant.

For pensions I needed to figure out my contribution plus what was added, for charity I just need to give my own contribution. Obviously. Still, this number is easy to find in my records.6

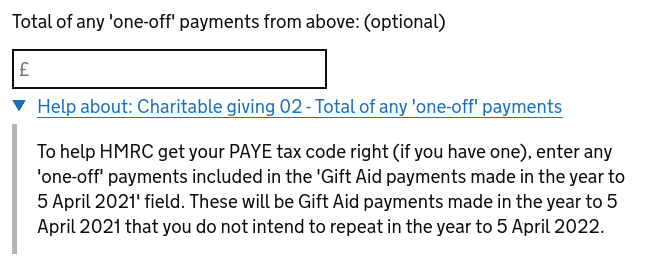

I think this is a roundabout way of asking how much gift aid I expect to donate in tax years 2021-22 and/or 22-23? They'll assume it's the amount I donated this year, minus whatever I put here. And then they'll adjust my PAYG tax code for that, to reduce overpayments.

Most of my charity donations were monthly recurring, but that left me slightly below my "10% of take-home" target, so I did do a one-off donation on top of that which I don't particularly expect to repeat. (But I haven't checked how far below my target I am right now.) But I do expect to donate more in total this year, so I'm going to leave this blank.

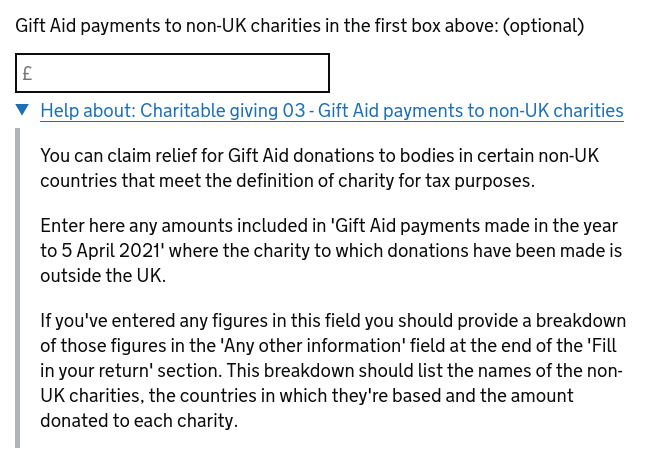

Not much help about what specific countries count as "certain" here, or what the definition of charity is for tax purposes. Some of the money I donate goes to MIRI, which is not a UK charity. But it goes via EA Funds, which is. So I'm pretty sure I haven't officially done this.

I can ignore the rest: I'm not asking to treat any payments as being made in a year other than they were actually made; and I haven't given any shares, securities, land or buildings to charity.

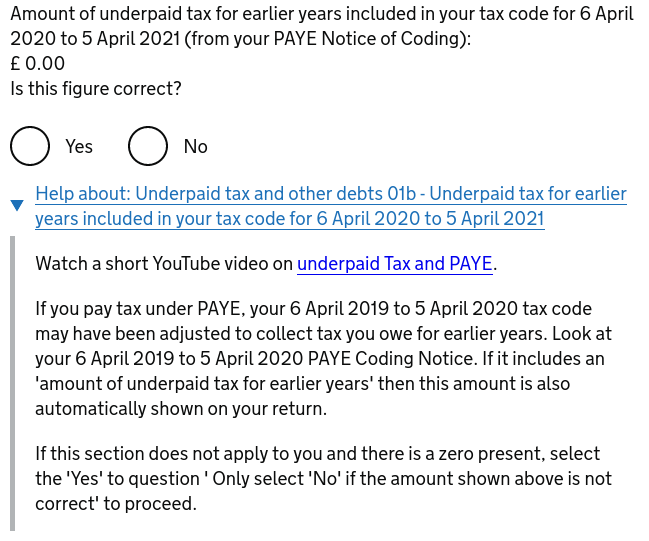

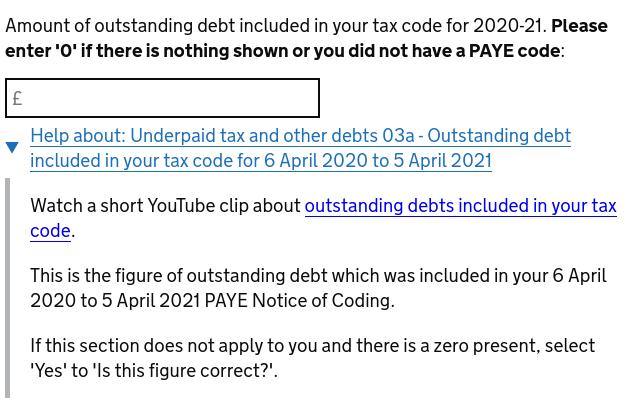

The next three pages are about my "PAYE Notice of Coding". They never say what one of these is, but it seems to be a letter they send out, that as far as I can see doesn't contain the words "PAYE" or "notice of coding". (It does say "your tax code notice", which is at least similar.)

Awkwardly, I can't find one more recent than 2018-19: not in my physical documents box, my "I should look through these documents at some point" pile, or my email. I'm sure I've had them more recently, so, um. They don't tell me what to do in this situation, but I guess presumably I can ask them for a new one? But… look at these questions.

The first is "does this number match what's on your coding notice?"

It's not clear whether it's talking about 2019-20 or 2020-21. If I had to guess - and I suppose I kind of do? Then I'd guess it's asking about underpaid tax from 2019-20 and earlier that I should have paid back in 2020-21 through my tax code for 2020-21.

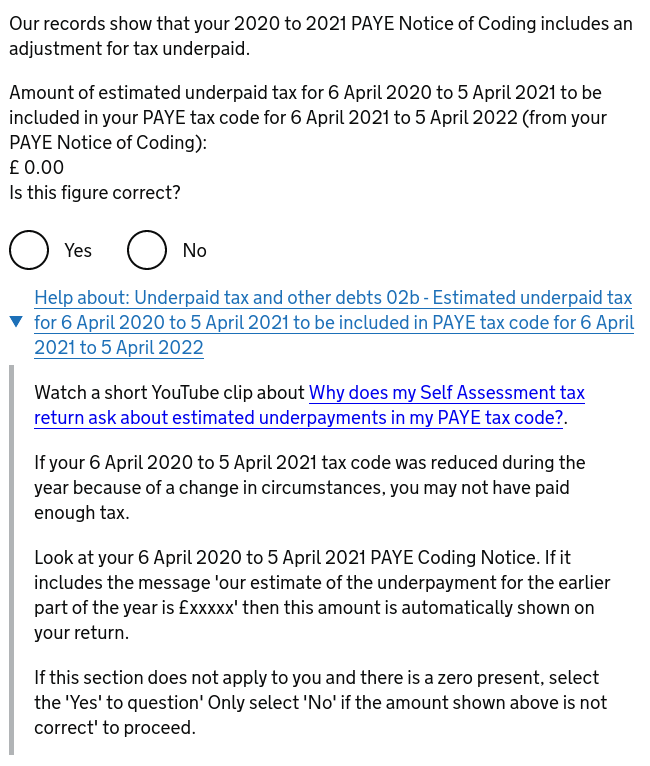

The second is also "does this number match what's on your coding notice?" I think the difference is that last one was talking about underpaid tax from previous years, and this one is talking about underpaid tax from 2020-21 that's already been put on my 2020-21 tax code.

(For these, if I select "no" I get a space to put a different number and a space to tell them where that other number comes from.)

The third question doesn't look like the first two, although it does in the linked video and the help text sounds like it should. It's another "does this number match what's on your coding notice?" This time it's about… outstanding debts other than underpaid tax? What else might I owe to HMRC?

So, okay. I confess I don't really know what's going on with any of this. But suppose I ask HMRC for a replacement Notice of Coding. Are they really going to give me a letter telling me a different number than they have on the website? If so, why not just take that number from wherever they got it for the letter, and put it on the website themselves?

Plus, I've received tax refunds the last two years running, which seems like a weird thing to get if they think I owe them money?

So I think I'm just gonna assume these are all £0.

The three linked videos are short (1:15 to 2:07), but they don't add much that's not in the help text, and I'd much rather they be presented as "text with embedded images" or even just plain text. At least they have subtitles.

Nearly done! Quickfire round.

The next page is one I can't do anything with until after I've submitted the return. This seems like a strange place for it.

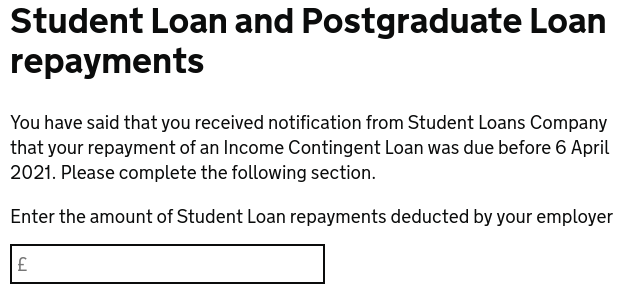

Then we get a page about my student loan, which doesn't even have a help text. This is on my P60 again, and also I have it in my own records and I'm pretty sure on a letter somewhere.

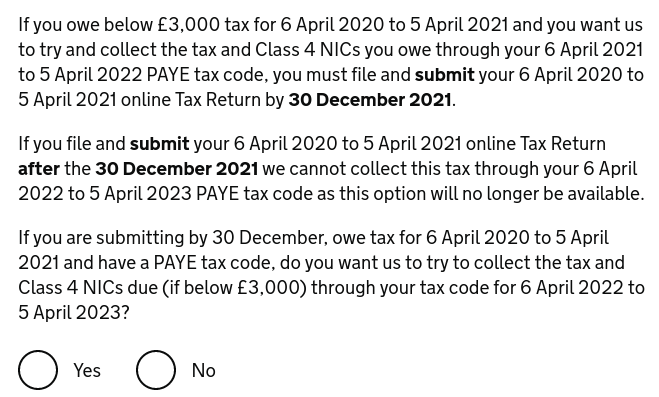

Next they have two questions about underpaid tax.

The first is: if it turns out I didn't pay enough tax last year (2020-21, the year I'm filing for), do I want to pay it back through my tax code for next year (2022-23)? i.e. to get it automatically deducted from my payslip starting April 2022? That seems reasonable, sure. If I say no I have to pay it directly by January 2022. I think it's more likely I paid too much, but gonna say yes anyway.

I can only do this if I file by 30th December, which is (checks calendar) soon. I guess if this guide does turn out to be useful to someone, they won't be able to take advantage of this, this year.

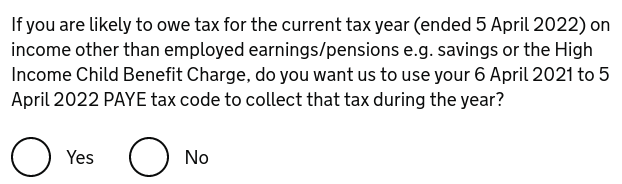

The second is: if they think I'll owe7 tax this year (2021-22, the unfinished year I'm writing this), do I want it put onto my tax code for… also this year? But this doesn't apply to tax on employed earnings (i.e. the only thing I think I owe tax on) or pensions. Also they apparently think 5 April 2022 gets the past tense.

So, no, because I don't think I'll owe the relevant kind of tax, and if they decide I probably will that's going to confuse things. And no again, because if they decide I'll probably owe something, putting it on my tax code for this year (with three payslips to go) also seems like it's going to confuse things. Certainly it'll make updating my ledger mildly less convenient. If I was going to do this, I'd rather it go on my tax code for next year, like with the previous question.

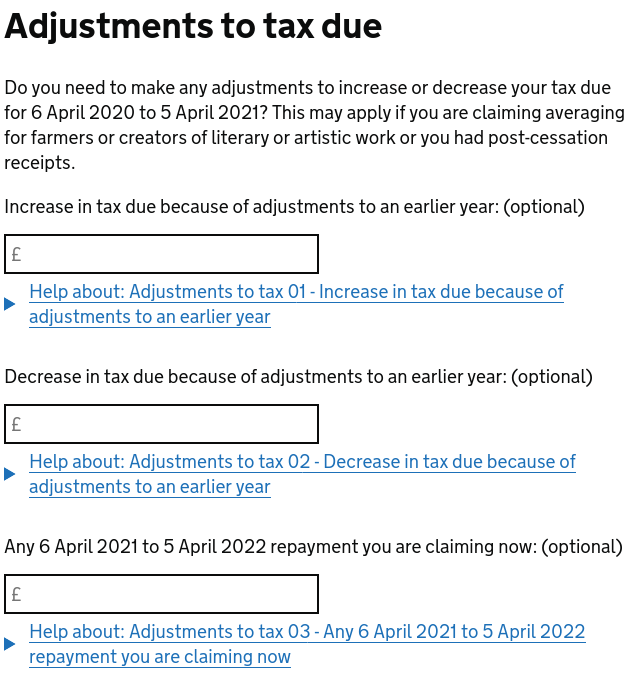

If I want to make "adjustments" I can do that, but I don't think it applies. (It sounds like these adjustments might be mostly "pretending things happened at different times than they actually happened"?)

The help texts all include "An entry will only be required in limited circumstances", and make it sound like calculating the amounts to go in these boxes is kind of complicated, so I'm glad I don't have to think about them.

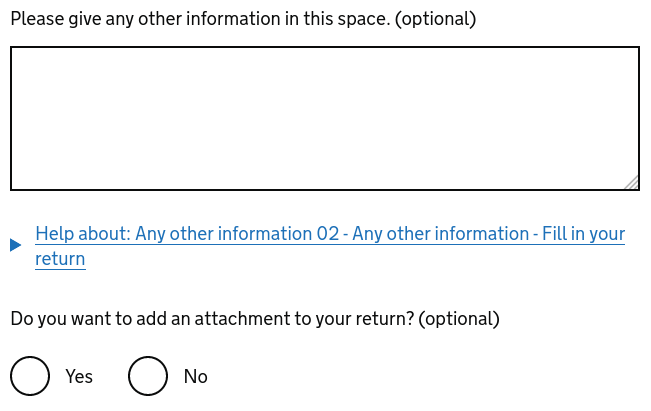

If I used provisional figures (I didn't) I give them details about those, and then finally there's a space for "anything else we should know" with the same restrictions on length and punctuation as before. Also I can attach a document if I want.

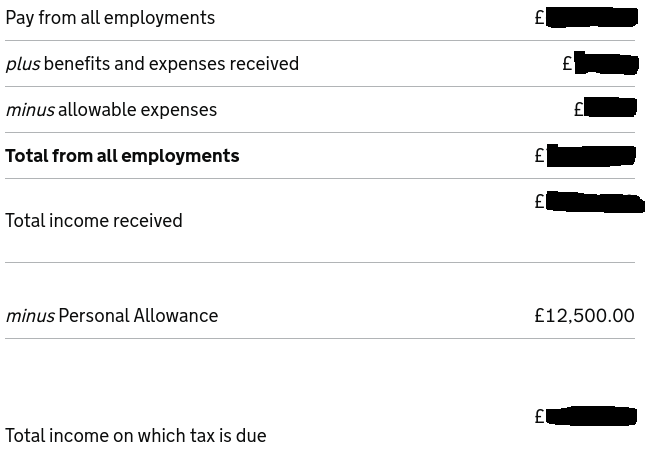

That's the last thing to fill in. Next there's a page where they repeat some of the things I said back to me, to confirm, and then a page to show me my tax calculation. Initially it just says how much they owe me (or presumably, how much I'd owe them, if that was the case). But then there's also a page showing the full calculation, which I find super valuable for understanding how it all fits together and double checking that I haven't made any mistakes.

The top three numbers here come directly from my return, and Personal Allowance is the same for most people, £12,500 for 2020-21. (If you earn over £100k it starts to decrease, giving a marginal 60% tax band in between two marginal 40% tax bands. I guess it was politically easier to raise taxes this way than to raise them in some more sensible way?) The rest are just adding and subtracting those numbers in the obvious way.

Normally, of the "income on which tax is due", I'd pay 20% on the first £37,500 and 40% on the rest. But

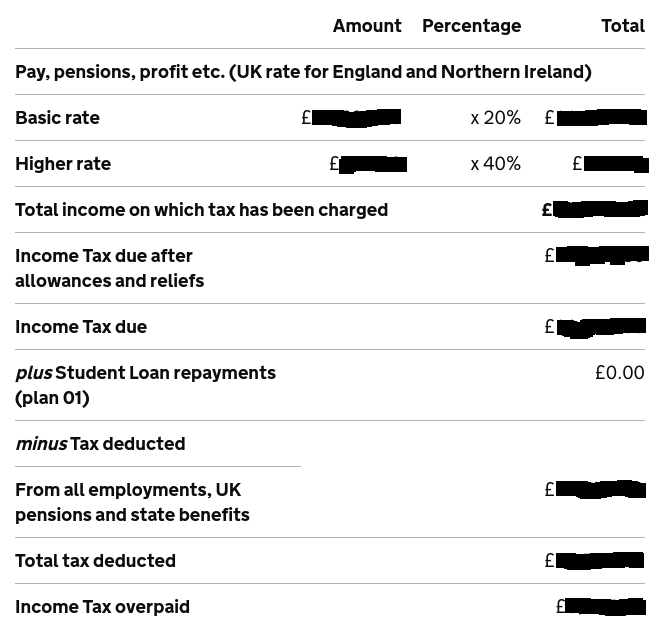

The pension number is the amount I put in the first pension box above, "payments to registered pension schemes". That was money I'd paid into my pensions, plus tax relief I'd been given for it.

The charity number is the amount of gift aid payments I made, times 1.25, because the number I entered didn't include tax relief. (That tax relief went to the charities, not to me.)

The idea with these is that money I put into pensions, or give to charity, is money I don't have to pay tax on. So they make two adjustments for it:

-

Return 25% of the money I deposit/donate, to me (for pensions) or the charity (for charities). This happens without needing to fill in a tax return. For those in the basic rate tax bracket, it gives the right amount - £100 pre-tax becomes £80 post-tax, so later we turn the £80 back into £100.

-

For higher rate taxpayers, also move some money from the "pay 40% tax" bucket to the "pay 20% tax" bucket. £100 pre-tax becomes £60 post-tax, which (from the previous point) becomes £75 when moved to the pension pot or charity. So they move £75 between buckets, and instead of paying £30 on that I now pay £15. So of the original £100, I now have £15, the charity has £75, and HMRC has £10. This is the same as me giving the charity £75 pre-tax and then paying 40% tax on £25, so it works out fine, but man I find this math confusing.

If I actually want to give £100 pre-tax, I still need to give the charity £80. They'll claim back £20 and so will I, so I'll have given them £100 pre-tax and paid 40% tax on £33.33. Alternatively I can take the £15 I got returned from £60 and redonate that, becoming £18.75 to the charity, then also donate the £3.75 I get returned from that, and so on - in the limit, this works out as the charity having £100 and myself and HMRC having £0 each.

(When HMRC shifts money between buckets, a higher-rate taxpayer can become a basic-rate taxpayer. I assume the math still works out fine at the boundaries? I haven't checked though.)

And so we have these calculations:

I'm not sure why "Income Tax due after allowances and reliefs" comes before "Income Tax due", but since I don't have any allowances or reliefs the numbers are the same for me. I assume student loan repayments would be different from £0 if the wrong amount had been automatically taken from my payslips.

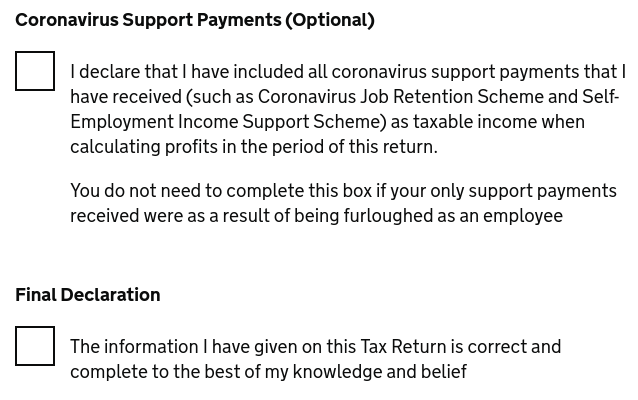

Now I get to download a PDF copy of what I just filled in, formatted on what I guess is a copy of the paper form I'd use if I wasn't doing it online. And then right before I submit, two more checkboxes to tick:

This first one seems less helpful than it might be, failing to distinguish "oops I did this wrong" from "I didn't need to do this". I guess they don't want to confuse non-mathematicians who didn't have any coronavirus support payments, and it still works as a reminder.

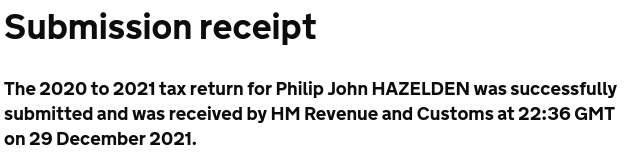

I think after I click "submit" on this page, I'll enter my password again and be finished. But I haven't done that yet - I'll wait to see if anyone wants to tell me I did something wrong, first.

Update December 29: Yep, that was it. There was a "submitting" spinner for about 30 seconds, and then

Woop! It takes up to 72 hours to process and I can make corrections in that time. But assuming I don't realize I have any of those, I'm done. At some point they're going to send me back the money I overpaid, historically that's gone into my bank account but I don't remember if I've had to do anything particular to make it happen. Certainly it wasn't very involved if I did.

They give me a "submission receipt reference number", which looks like 32 digits in base 36 (numbers and uppercase letters, mine includes Z, I and O so probably all letters are possible). Sounds like it's a hash of the contents of my return, with a signature so that no one else can generate a valid one. Neat. It's also included in the PDF copy I downloaded earlier.

I assume it's not intended to be confidential, but they don't say it's safe to share, so I won't.

-

In this context. ↩

-

In the current tax year I've done a small amount of trading, because I couldn't directly buy the thing I wanted to. My vague impression is that because I bought and traded on the same day I can ignore this? (I'm not sure where I heard that. If it's true, I wonder if it's also true for high-frequency traders.) But also we're talking amounts small enough that I'm not going to reach either threshold this tax year, whether I can ignore this or not. ↩

-

The only thing I think I've used the SA150 for, is to confirm that this is correct. ↩

-

When I switched ISP, there was a week when my new one failed to connect me and I had to use mobile data for internet. As it happens I didn't use more than my contracted amount, but if I had… strictly it doesn't sound like that would be covered? I kind of guess I'd be able to claim for some of it, even though this page only mentions dial-up, but I'm not sure. ↩

-

I assume this means something like "reasonably compelling evidence that I spent the amount I claim to have spent". Strictly speaking, if I said "I spent £10/week extra" that would be evidence I spent £10/week extra, because I'm a fairly honest person (citation needed) and I am more likely to say something if that thing is true than if it is false. But I somehow feel like HMRC would not accept this evidence. ↩

-

I track my finances with Ledger, and apply a tag to all gift aided charity contributions. ↩

-

I think "owe" here means gross, not net. That is, the question isn't "will I have paid less tax in these buckets than I'm required to", which I don't think is a question that makes sense after I've paid any tax at all. (When I pay tax it doesn't offset specific tax buckets, it just offsets my total tax bill.) Rather, the question is "will the amount I'm required to pay in these buckets be more than £0". This is a different use of the word "owe" than in the previous question, but ¯\_(ツ)_/¯ ↩

Posted on 28 December 2021

Tagged: practical

Comments elsewhere: /r/UKPersonalFinance